The start of a new financial year is the perfect time to review your business finances and ensure you’re up to date with the latest Australian Taxation Office (ATO) requirements.

Keeping on top of tax and compliance changes not only helps your business avoid penalties, but also creates opportunities to improve cash flow, maximise tax deductions and make better financial decisions throughout the year.

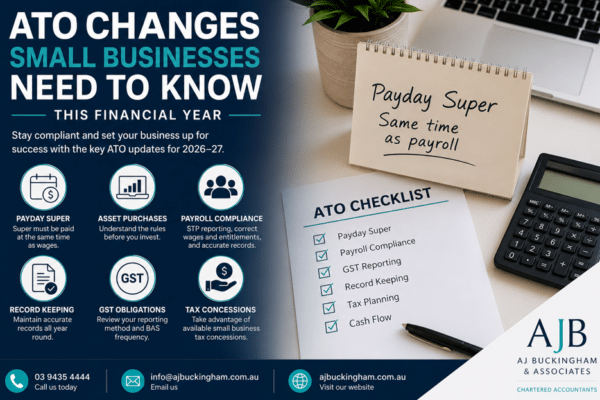

Whether you’re a sole trader, company or family business, here are the key ATO changes and compliance areas every small business should be aware of this financial year.

1. Payday Super Is Now in Effect (Super Must Be Paid Each Pay Run)

One of the most significant changes for employers is the introduction of Payday Super, which fundamentally changes how and when superannuation must be paid.

Under the new rules, superannuation is no longer something that can be set aside and paid quarterly. Instead, super must now be calculated, processed and paid at the same time as each payroll cycle.

This means that every time you run payroll—weekly, fortnightly or monthly—superannuation contributions must be submitted at the same time, not left until later.

What this means in practice:

- Super is processed with every pay run, not separately

- Contributions must be sent to funds within the required timeframe after payroll is completed

- Payroll systems must be configured to calculate and process super automatically per pay cycle

- Delayed or separate super payments may result in compliance issues or penalties

This change is designed to improve retirement outcomes for employees, but it also means businesses must have tighter payroll processes and more accurate cash flow planning.

What you should do now:

- Ensure your payroll software is fully configured for Payday Super

- Confirm super is being calculated and processed at the same time as wages

- Review your payroll workflow to ensure super is not treated as a quarterly task

- Check that payment timing aligns with ATO requirements after each pay run

If your business is still treating super as a quarterly obligation, immediate process changes are required to remain compliant.

2. Review Your Asset Purchase Plans

If you’re planning to purchase equipment, vehicles, machinery or technology this financial year, it’s important to understand the current tax treatment of business assets.

Depending on current tax legislation, eligible businesses may be able to claim deductions for qualifying business assets. However, these rules can change from year to year, making professional advice essential before making significant purchases.

Planning your investments carefully can improve cash flow while ensuring you receive the maximum available tax benefits.

3. Stay on Top of Payroll Compliance

Payroll compliance continues to be an area of focus for the ATO.

In addition to Payday Super requirements, businesses should ensure they are:

- Reporting correctly through Single Touch Payroll (STP)

- Paying employees the correct wages and entitlements

- Meeting all leave and award obligations

- Keeping employee records accurate and up to date

A payroll review at the start of the financial year can help identify issues early and reduce compliance risk.

4. Maintain Accurate Business Records

Good record keeping remains one of the simplest ways to stay compliant and reduce stress at tax time.

Your business should maintain accurate records for:

- Income and sales

- Business expenses

- GST transactions

- Payroll records (including super paid each pay cycle)

- Vehicle and travel expenses

- Asset purchases

Cloud accounting software can make record keeping more efficient while providing real-time insight into your business performance.

5. Review Your GST Obligations

The start of the financial year is an ideal time to review your GST reporting processes.

Consider:

- Whether your BAS reporting method is still appropriate

- If your bookkeeping is up to date and accurate

- Whether GST is being recorded correctly on all transactions

- If your reporting frequency supports your cash flow needs

Small improvements in GST processes can reduce errors and improve financial clarity.

6. Understand Superannuation as a Real-Time Payroll Cost

With Payday Super now in place, superannuation is no longer a periodic obligation—it is a real-time payroll cost that must be factored into every pay run.

This means businesses should:

- Budget super as part of each payroll cycle

- Treat super as a direct cost of wages, not a separate quarterly bill

- Adjust cash flow forecasting to reflect more frequent outflows

- Ensure payroll and accounting systems are aligned

This shift makes payroll more transparent but also requires stronger cash flow discipline throughout the year.

7. Don’t Miss Available Tax Concessions

Small businesses may still be eligible for a range of tax concessions depending on their circumstances, including:

- Small business depreciation rules

- Capital gains tax (CGT) concessions

- Simplified accounting methods

- Other available small business tax relief measures

Understanding which concessions apply can significantly reduce tax payable and improve business outcomes.

8. Manage Your Cash Flow for Tax Obligations

One of the biggest challenges for small businesses is ensuring enough cash is set aside for tax obligations.

Businesses should regularly allocate funds for:

- GST

- PAYG withholding

- Superannuation (now per pay run)

- Income tax

With Payday Super increasing the frequency of super payments, strong cash flow forecasting is more important than ever.

Practical Steps to Stay Compliant

To stay ahead of ATO requirements this financial year:

- Review payroll and accounting systems for Payday Super readiness

- Ensure super is processed at the same time as each payroll cycle

- Maintain accurate and up-to-date records

- Schedule regular financial reviews

- Speak with your accountant before major financial decisions

Partner with Trusted Business Advisers

At AJ Buckingham & Associates, we help small businesses adapt to changing ATO requirements with confidence and clarity.

Our team provides practical support in:

- Payroll and Payday Super compliance

- Tax planning and structuring

- Cash flow management

- Business advisory and growth planning

- GST and BAS compliance

If you’d like help reviewing your payroll systems or ensuring your business is compliant this financial year, call us on 03 9435 4444 to book a consultation.

{kind=link}