1. The Government’s Three Stage Personal Income Tax Plan

The Government is introducing a 7 year Personal Income Tax Plan that will be rolled out in three stages. The first stage of the Tax Plan will provide Australian resident low and middle income earners with a non-refundable tax offset of up to $530 per annum. The offset will be received as a lump sum on assessment after an individual lodges their tax return. The offset will be available from 2018/19 through to 2021/22.

- For Low and Middle Income Earners with taxable incomes of $37,000 or less, the tax offset will provide an annual benefit of up to $200.

- For Low and Middle Income Earners with taxable incomes between $37,001 and $48,000, the value of the tax offset will increase at a rate of 3 cents per dollar to the maximum annual benefit of $530.

- Taxpayers with Taxable Incomes from $48,001 to $90,000 will be eligible for the maximum annual benefit of $530.

- For taxpayers with taxable incomes from $90,001 to $125,333, the offset will be phased out at a rate of 1.5 cents per dollar earned in excess of $90,000.

Importantly, the Government has proposed the Low and Middle Income Tax Offset is in addition to the current Low Income Tax Offset.

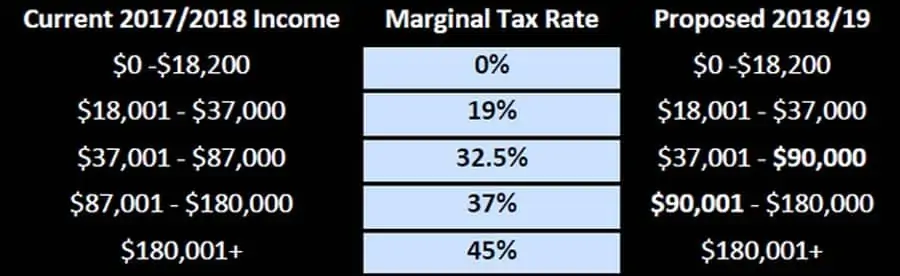

Stage 2: Preventing Bracket Creep

The Government has proposed the following tax rates for individuals:

As the table illustrates, from 1 July 2018, the top taxable income threshold of the 32.5% personal income tax bracket will be increased from $87,000 to $90,000.

From 1 July 2022, the top taxable income threshold for the 32.5% personal income tax bracket will be increased from $90,000 to $120,000. The top taxable income threshold for the 19% personal income tax bracket will be increased from $37,000 to $41,000. From 1 July 2022, the Low Income Tax Offset will be increased from $445 to $645.

Stage 3: Removal of the 37% Tax Bracket Entirely

From 1 July 2024 the Government will simplify and flatten the personal tax system by removing the 37% tax bracket altogether by increasing the top taxable income threshold of the 32.5% personal income tax bracket from $120,000 to $200,000. This is in recognition of inflation and wage growth. The new 32.5% tax bracket will incorporate taxable incomes from $41,001 to $200,000. Taxpayers with taxable incomes exceeding $200,000 will pay the top marginal tax rate of 45%. That is, the top marginal tax rate will be payable on taxable incomes from $200,000 instead of the current $180,000.

2. The Medicare Levy

The Government will retain the Medicare levy rate at 2% of taxable income for eligible taxpayers and not increase it to 2.5% as previously proposed to assist in funding the NDIS. Changes to other tax rates that are linked to the top personal tax rate, such as the fringe benefits tax rate, will also not proceed.

The Government will increase the Medicare levy low-income thresholds for singles, families, seniors and pensioners from the 2017/18 income year as follows:

3. Taxation of High Profile Individuals

From 1 July 2019, the Government will ensure that high profile individuals will no longer be able to take advantage of lower tax rates by licencing their fame or image to another entity. Under the current tax environment, high profile individuals such as sports people and actors can licence their fame or image to another entity such as a related company or trust. All income derived under this licence is assessable income to the entity that holds the licence. This has allowed these individuals to spread their income to decrease the rate of tax paid. The new proposal will ensure that all remuneration, including payments and non-cash benefits provided for the commercial exploitation of a person’s fame or image, will be included in the assessable income of that individual.

{kind=link}