Treasurer Josh Frydenberg presented his second budget on October 6 in what was described as the, “most important budget since World War II”. As expected, there is massive expenditure to reboot and stimulate the economy after the economic devastation brought on by the coronavirus pandemic.

The Budget outlined $85 billion of stimulus over four years, which is centred around immediate asset write-offs, income tax cuts and the extension of JobKeeper.

The Treasurer promised a budget that was “all about jobs”, and employment is indeed the theme of the suite of budget measures. For small and medium businesses, this translates to new wage subsidies for hiring young job-seekers and new apprentices, albeit with tight eligibility criteria. The Treasurer said, “There is no economic recovery without a jobs recovery,” and “There is no budget recovery without a jobs recovery.”

Frydenberg’s goal is to get businesses investing again, in new equipment and machinery, and new jobs. To this end, the government has announced a massive investment allowance that will enable nearly all Australian businesses to fully write-off all new assets purchased and used by June 2022.

We have summarised some of the key budget announcements including:

- the bringing forward of the individual tax relief planned for 2021, backdated to 1 July 2020

- a new loss carry-back for losses incurred up to June 2022 for companies with turnovers of up to $5 billion allowing most businesses to fully deduct any investment into depreciable assets until 30 June 2022, and

- a new JobMaker Hiring Credit for companies employing staff aged between 16 to 35 years old.

Personal Income Tax

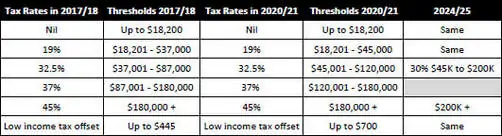

As part of the Government’s JobMaker Plan, the tax cuts originally planned for July 2022 will be brought forward and backdated to July 1, 2020. They have lifted the threshold for the 19 per cent tax rate to $45,000 and the 32.5 per cent threshold to $120,000. The low and middle-income tax offset will also remain.

The Government’s Personal Income Tax Plan was designed to lower personal taxation and was to be implemented in three stages with Stage 1 implemented in June 2018. Stage 2 was to commence in 2021, however, this budget brings forward those tax cuts as well as a one-off additional benefit from the low and middle income tax offset in 2020/21. Stage 3 of the Government’s Personal Income Tax Plan remains in place for roll-out in 2024/25.

In 2020/21, low and middle income earners will receive tax relief of up to $2,745 for singles, and up to $5,490 for dual income families, compared with the 2017/18 rates. The majority of the tax benefit for 2020/21 will go to those on incomes below $90,000. Refer to the table below.

Tax Rate & Thresholds In 2017/18 Compared To 2020/21

Tax Relief Based On Taxable Income In 2020-21 Compared To 2017/18

![]()

Superannuation

The Government has announced that, from July 1, 2021 they will implement a proposal to ‘staple’ an existing superannuation account to an individual as they move between jobs. The purpose of this measure is to reduce duplication of superannuation accounts for individuals when they change jobs and do not nominate their existing fund with their new employer (or otherwise do not consolidate their super if a new account is created for them).

This is a welcomed measure which reflects a proposal recently made by the Productivity Commission. We expect that the changes will improve the employee onboarding process for both employees and employers, and that future enhancements to payroll software will further simplify administrative processes on commencement of employment.

Business Taxation

Generally speaking, a business asset is ’depreciated’, meaning that a portion of the cost of the asset is deductible each year over the life of the asset. Under this measure, businesses with aggregated annual turnover of less than $5 billion will be able to deduct the full cost of eligible capital assets acquired from 7:30pm AEDT on 6 October2020 (Budget night) and first used or installed by June 30, 2022.

Full expensing of the asset in the year of first use will apply to new depreciable assets and the cost of improvements to existing eligible assets. For small and medium sized businesses (with aggregated annual turnover of less than $50 million), full expensing will also apply to second-hand assets. The budget papers do not specify details of which assets will be ‘eligible’ assets for the purposes of this measure, but we expect that the definition will be broad.

The ‘immediate expensing’ applies to assets acquired after October 6, 2020. However, there is also an extension for businesses that acquired assets before budget night but had not yet used or installed them. Businesses that hold assets eligible for the enhanced $150,000 instant asset write-off will have an extra six months, until June 30, 2021, to first use or install those assets. Small businesses (with aggregated annual turnover of less than $10 million) can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies. The provisions which prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended.

The benefits for your business:

- Immediate deductions for capital investments in assets to reduce the taxable income of the business in the year the asset is purchased

- Deductions allowed on an asset by asset basis

- Deductions for depreciation pool balances (i.e. immediate tax deduction for costs that would previously have been claimed over several years)

- If increased deductions for capital investments contribute to a company’s tax loss position, electing to apply the loss carry back provisions may allow the company to obtain a tax refund.

The Government will allow eligible companies to carry back tax losses from the 2020, 2021 or 2022 financial years to offset previously taxed profits in 2019 or earlier income years.

Corporate tax entities with an aggregated turnover of less than $5 billion can apply tax losses against taxed profits in a previous year, generating a refundable tax offset in the year in which the loss is made. The tax refund will be available on election by eligible businesses when they lodge their 2021 and 2022 income tax returns. Currently, companies are required to carry forward tax losses to offset them against profits in future years. Companies that do not elect to carry back losses under this measure can still carry forward losses as normal.

The tax refund will be limited by requiring that the amount carried back is not more than the earlier taxed profits and that the carry back does not generate a franking account deficit. In other words, the tax refund generated by the loss carry back provisions cannot exceed the company’s franking account balance.

This measure is designed to promote economic recovery by providing cash flow support to previously profitable companies that have fallen into a tax loss position as a result of the currently weaker economic conditions.

The loss carry-back provisions will also support the incentive for companies to invest under the investment incentive measures which will temporarily allow full expensing of capital acquisitions. If increased deductions for capital investments contribute to a company’s tax loss position, electing to apply the loss carry back provisions may allow the company to obtain a tax refund.

The Government is introducing an incentive to encourage organisations to take on additional employees. This new incentive, the JobMaker Hiring Credit, will be available to eligible employers over 12 months from 7 October 2020 to 6 October 2021 for each additional new job they create for an eligible employee.

Employer Eligibility – Eligible employers who can demonstrate that the new employee will increase overall employee headcount and payroll will receive:

- $200 per week if they hire an eligible employee aged 16 to 29 years or

- $100 per week if they hire an eligible employee aged 30 to 35 years.

The JobMaker Hiring Credit will be available for up to 12 months from the date of employment of the eligible employee with a maximum amount of $10,400 per additional new position created. Most employers would be eligible, however, employers must have an Australian Business Number (ABN), be up to date with their tax lodgement obligations, be registered for Pay As You Go (PAYG) withholding, report through Single Touch Payroll (STP) and cannot be claiming the JobKeeper Payment.

Employee Eligibility – To attract the JobMaker Hiring Credit, the employee must be in an additional job created from 7 October 2020. To demonstrate that the job is additional, specific criteria must be met. There must be an increase in:

- the business’ total employee headcount (minimum of one additional employee) from the reference date of 30 September 2020; and

- the payroll of the business for the reporting period, as compared to the three months to 30 September 2020.

The amount of the hiring credit claim cannot exceed the amount of the increase in payroll for the reporting period. To be eligible, the employee will need to have worked for a minimum of 20 hours per week, averaged over a quarter, and received the JobSeeker Payment, Youth Allowance (other) or Parenting Payment for at least one month out of the three months prior to when they are hired.

How to claim the Jobmaker Hiring Credit

The JobMaker Hiring Credit will be claimed quarterly in arrears by the employer from the Australian Taxation Office (ATO) from 1 February 2021. Employers will need to report quarterly that they meet the eligibility criteria.

The Government will expand access to a range of small business tax concessions by increasing the small business entity (SBE) turnover threshold for these concessions from $10 million to $50 million. Businesses with an aggregated annual turnover of $10 million or more but less than $50 million will for the first time have access to up to ten further small business tax concessions in three phases:

- From 1 July 2020, eligible businesses will be able to immediately deduct certain start-up expenses and certain prepaid expenditure.

- From 1 April 2021, eligible businesses will be exempt from the 47 per cent fringe benefits tax on car parking and multiple work-related portable electronic devices (such as phones or laptops) provided to employees.

- From 1 July 2021, eligible businesses will be able to access the simplified trading stock rules, remit pay as you go (PAYG) instalments based on GDP adjusted notional tax, and settle excise

Eligible businesses will also have a two-year amendment period apply to income tax assessments for income years starting from 1 July 2021, excluding entities that have significant international tax dealings or particularly complex affairs. The eligibility turnover thresholds for other small business tax concessions will remain at their current levels.

The federal government will allocate $420 million in this year’s budget to accelerate its plans to create a single national business registry, in a move designed to cut red tape for small business operators. The super registry will be operated by the Australian Taxation Office and will bring together the Australian Business Register and 31 other registers currently administered by the Australian Securities and Investments Commission.

{kind=link}