As we approach the end of the 2024–25 financial year, it’s not only about exploring tax-saving strategies—it’s also essential to meet all year-end compliance obligations. Part 2 of our 2025 Tax Planning Guide outlines important matters not covered in Part 1, including superannuation changes, motor vehicle log books, trust resolutions, Division 7A loan repayments, stock valuations, and more.

Staying on top of these items can significantly reduce your tax liability and help you avoid costly penalties.

🔺 Super Guarantee Rate Increase – Be Prepared

From 1 July 2025, the Super Guarantee Contribution (SGC) rate increases from 11.5% to 12%. Employers should budget now for this rise in compulsory super contributions.

✅ Extra Year-End Compliance Checklist

In addition to the tax planning opportunities, there are several obligations in relation to the end of the financial year which should be considered:

🚗 Motor Vehicle Logbooks

If you use a vehicle for business purposes:

- Record your odometer reading as at 30 June 2025.

- Prepare a logbook for 12 continuous weeks if your existing one is more than 5 years old. Please note, if you commence the logbook prior to June 30, 2025, the usage determined will still be appropriate for the whole of 2024/25. As such, it is not too late to start preparing one for the current financial year.

If you are in business or earn your income through a Company or Trust:

💼 Employer Superannuation Obligations

- Final SGC Payment Deadline: 28 July 2025.

- Tax Deduction Cut-Off: For deductibility in 2024/25, super contributions must be received by the fund (or ATO Small Business Clearing House) by 30 June 2025.

Avoid last-minute payments—processing delays could cost you your deduction.

🔄 Division 7A Loans – Private Companies

If you’ve borrowed funds from your company:

- Ensure loan repayments (principal & interest) are made by 30 June 2025.

- For new loans this year, ensure either:

- The loan is fully repaid, or

- A complying Division 7A loan agreement is executed before your company’s tax return is due.

- The loan is fully repaid, or

Non-compliance may result in the loan being treated as an unfranked dividend in your personal return.

🧾 Trustee Resolutions

Trustees of Discretionary (Family) Trusts must:

- Finalise and sign trust distribution resolutions before 30 June 2025. Ensure that the Trustee Resolutions on how the income from the trust is distributed to the beneficiaries are prepared and signed before June 30, 2025, for all Discretionary (“Family”) Trusts.

Failure to do so means the trust income may be taxed at the top marginal rate, or automatically distributed to default beneficiaries.

📋 Stock Count & Valuation

- Complete a stocktake and working papers as of 30 June 2025.

- Value stock at the lower of cost or net realisable value.

Write down obsolete or unsellable stock to reflect actual market value.

🧾 Reconciliation of PAYG & Finalisation

- You are not required to issue PAYG payment summaries for amounts reported and finalised through Single Touch Payroll (STP).

- Ensure all payroll data is finalised in your software, and lodge your STP Finalisation Declaration.

🏢 Company Tax Rate for Small Business

The 2025 company tax rate for base rate entities is 25%, if:

- Annual aggregated turnover is under $50 million, and

- No more than 80% of assessable income is from passive sources.

🧠 Additional Tax Planning Considerations

Stock Valuation Options

- Review your Stock on Hand and Work in Progress listings before June 30 to ensure that it is valued at the lower of Cost or Net Realisable Value. Any stock that is carried at a value higher than you could realise on sale (after all costs associated with the sale) should be written down to that Net Realisable Value in your stock records.

🧾 Write Off Bad Debts

- If you report income on an accrual basis, write off bad debts before 30 June.

- A bad debt must be clearly recorded in your system to claim a deduction.

🔧 Repairs and Maintenance

- Bring forward necessary repairs and maintenance if cash flow allows.

Be aware of the distinction between deductible repairs and capital improvements—check with us if unsure.

🗑️ Obsolete Assets

- Scrap or decommission obsolete plant and equipment by 30 June to claim any remaining book value as a deduction.

💰 Superannuation Tax Planning Opportunities

Compulsory Superannuation Guarantee

If you want a tax deduction in the 2024/25 financial year, the superannuation fund must receive the funds by 30 June 2025. The Tax Office doesn’t consider a contribution to be made until the amount is actually credited to a super fund’s bank account so an electronic transfer to another bank account on June 30 is not necessarily considered paid. We strongly recommend you make the payment a week or so before June 30 and then follow up with the super fund to ensure the funds have been received. Don’t risk the tax deductibility of what can often be a significant amount by leaving payment to the last minute.

Concessional Contributions Cap of $30,000 for Everyone

The tax-deductible superannuation contribution limit or cap is $30,000 for all individuals regardless of their age for the 2024/25 financial year.

If eligible and appropriate, consider making the most of your 2024/25 financial year annual concessional contributions cap with a concessional contribution. Note that other contributions such as employer Superannuation Guarantee Contributions (SGC) and salary sacrifice contributions will have already used up part of your concessional contributions cap.

Carry Forward Concessional Contributions

If your total superannuation balance as of June 30, 2024, was less than $500,000 you may be able to carry- forward unused concessional caps for up to 5 years.

Members can access their unused concessional contributions caps on a rolling basis for five years and amounts carried forward that have not been used after five years will expire.

Typically, self-employed individuals and those who earn their income primarily from passive sources like investments make their super contributions close to the end of the financial year to claim a tax deduction. However, individuals who are employees may also use this strategy and those who might want to take advantage of this opportunity.

Non-Concessional Super Contributions

If eligible and appropriate, consider utilising all or part of your 2024/25 financial year annual non-concessional contributions cap by making a non-concessional contribution for up to $120,000 for the 2025 financial year or up to $360,000 over 3 years.

Government Co-Contribution to Your Superannuation

The Government co-contribution is designed to boost the superannuation savings of low and middle-income earners who earn at least 10% of their income from employment or running a business. If your income is within the thresholds listed below and you make a non-concessional contribution to your superannuation, you may be eligible for a government co-contribution of up to $500. earn $44,500 or less. A lower amount may be received if you contribute less than $1,000 and/or earn between $44,500 and $60,400. If unsure then ask your tax agent for clarification.

The matching rate is 50% of your contribution and additional eligibility include: having a total superannuation balance of less than $1.9 million on 30 June of the year before the year the contributions are being made having not exceeded your non-concessional contributions cap in the relevant financial year.

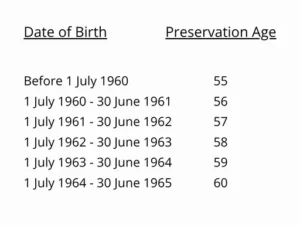

Transition to Retirement

If you don’t want to fully retire and would like to reduce your working hours you can take advantage of what is known as “Transition to Retirement” TTR. This means that providing you have reached your preservation age, see below, you can elect to keep working full time or part-time and take money out of your super to supplement your income. This is popular for those who want to scale down their working hours rather than retiring.

When you are receiving a TRT pension you can still work and claim a tax deduction for concessional contributions into your super up to $30,000 for the 2025 financial year.

If you decide to implement a TTR strategy, you must withdraw a minimum amount, currently 4% for someone aged 60 (based on age) from your superannuation account balance up to a maximum of 10%.

If you are under 60 any amount you withdraw will be subject to tax at your marginal rate of tax. You will also be entitled to receive a tax rebate of 15%. After the age of 60, the good news is that any amount you withdraw is TAX FREE!

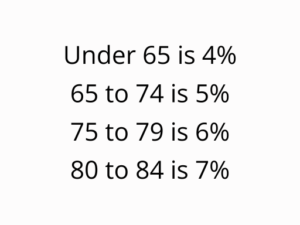

Account Based Pensions

If you are aged 60 + and retired or 65+ and still working, there are options worth considering. There are significant tax advantages in taking an Accountants Based Pension from your super. Not only are the withdrawals you make tax- free, but also the earnings within your superannuation fund are tax-free to 1.9 million dollars.

The minimum amount for ages:

To put in place an accounts-based pension, you will need to speak to your superannuation fund provider.

Summary:

With the Super Guarantee Contribution rate rising to 12% from 1 July 2025, businesses must prepare for several key year-end actions. These include recording vehicle odometers, finalising superannuation payments before 30 June for deductions, completing trust resolutions, and managing Division 7A loan repayments. Other considerations include stock valuation reviews, writing off bad debts, and scrapping obsolete assets. Superannuation strategies such as concessional and non-concessional contributions, carry-forward caps, and government co-contributions offer further planning opportunities. Transition-to-retirement and account-based pensions also provide tax-efficient retirement options. Planning and timely action can significantly impact your year-end tax position. Need help with year-end tax planning? Contact AJ Buckingham & Associates today to ensure you’re compliant and making the most of your tax and super opportunities.

{kind=link}